- Reg52

- Posts

- Why Natwest > Metro FCA Fine

FCC Insights

Hi ,

I’m prepping deep-dives on recent FCA actions against UK Retail Banks (Metro Bank, Santander, HSBC, NatWest).

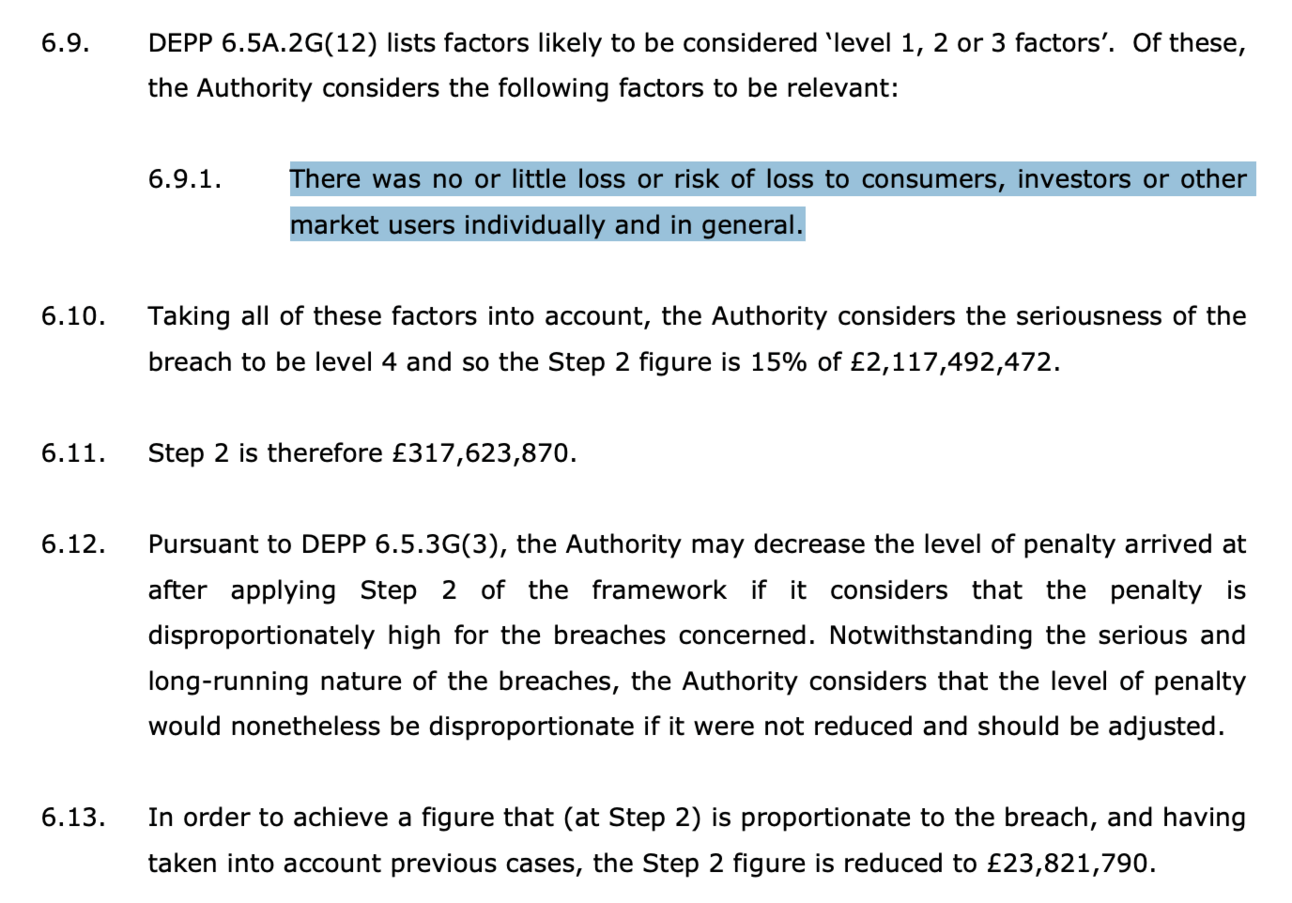

What’s really interesting are the comparisons between bank penalties.

Let’s dive into that today.

In similarities, all of the UK Banks mentioned above had serious issues with their Transaction Monitoring approaches.

Each were each fined for lack of alerts, or alert suppression or ignoring alerts (see below).

From HSBC Enforcement Action deep-dive to come

But in differences, when I look at this table one big question jumps out at me.

Why did NatWest get fined so much more than Metro Bank?

There were £365m of ignored alerts at NatWest; but

£51bn worth of un-monitored transactions at Metro Bank

The short answer is the “£ xbn un-monitored” numbers I pulled above are only one of a number of levers the FCA (or criminal court) pulls when setting a penalty.

So, what impact did each lever have for the NatWest and Metro Bank penalties?

Here’s the penalty calculation approaches across both cases with references - I’ve translated the Southwark Crown Court sentence to the FCA five penalty steps.

Lever in the penalty calculus | NatWest (2021) | Metro Bank (2023) |

|---|---|---|

Regime & forum | Criminal prosecution under MLR 2007 (Southwark Crown Court) - no upper statutory cap; sentencing guidelines emphasise deterrence (§111c) | |

Southwark Crown Court: Benefit gained FCA Step 1: Disgorgement | Disgorgement not stated in court decision but fees gained were £460k (§88) | No financial benefit derived from breach - £0 disgorgement (§6.3 & 6.4) |

Southwark Crown Court: Harm FCA Step 2: Seriousness | The Court found the best way was to measure harm was to consider how much money was paid into the offending accounts - ie £288m of the £365m highlighted above was during indictment period (§92) - and then applied a 40% reduction → revised penalty figure of £173m (§96) | FCA level 4/serious - 15 % of relevant revenue (§6.10) - relevant revenue was £2.1bn so this initial figure was £318m. But there is scope to reduce appropriately and this was thus reduced down to £23.8m - no reason given (§6.13) |

Southwark Crown Court: Category range adjustment for Aggravating & Mitigating Factors FCA Step 3: Aggravating and Mitigating Factors | No change for Aggravating & Mitigating & Medium culpability multiplier of 200% → adjusted figure now £345m (§110) | No increase or decrease based on these factors - stays at £23.8m (§6.18) |

Southwark Crown Court: Appropriate additional punishment, Deterrence & Totality FCA Step 4: Adjustment for Deterrence | 15% uplift to £345m = £397m (§127) | No change - stays at £23.8m (§6.21) |

Southwark Crown Court: Guilty plea FCA Step 5: Settlement Discount | 1/3 reduction due to guilty plea → 2/3 of £397m = £264.8m (§129) | 30 % early-settlement discount applied - £23.8m * 70% = £16.7m (§6.24) |

Total fine | £264.8 m | £16.7 m |

Key points

When you map out and compare penalty scoring approaches across cases and FCA/Courts, you can actually see that under the cloak of structure, there is a lot of subjectivity applied to penalties

The Metro Bank penalty could have been >£300m for the relevant revenue point but was reduced down by 92% (pasted below) from what I can see due to no customer, investor or market harm

Guilty plea/early settlement discounts have a huge impact (30-33% reduction)

Aggravating and Mitigating Factors often cancel each other out

When a case goes to court due to criminal behaviour the potential for penalties dramatically increases (by 10x+)

More to come in the individual deep-dives!

See you Friday.

Paul